Goldman Sachs Expands Private Credit Exposure as High Returns Raise Risk Questions

Goldman Sachs is generating strong returns from its lending to private credit firms and other non-bank financial institutions, but the strategy is drawing increased scrutiny as questions emerge over the balance between risk and reward.

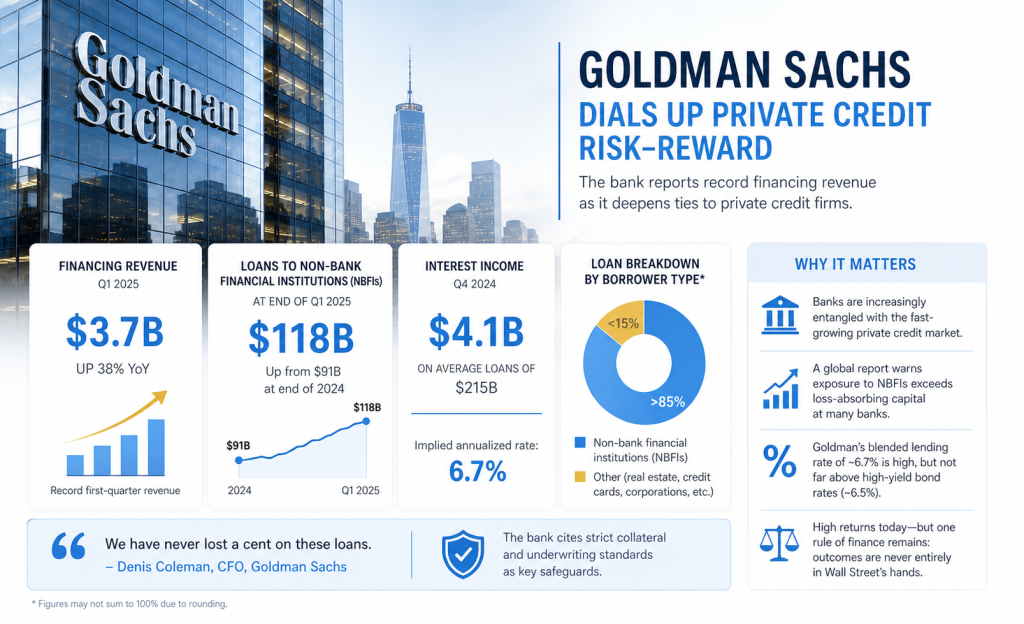

The Wall Street bank reported a record $3.7 billion in financing revenue in the first quarter, up 38% from a year earlier. Executives attributed part of the growth to heightened market volatility, which tends to boost lending activity, but also to the relatively high interest rates charged to clients operating in private markets.

Chief Executive David Solomon has described the firm’s lending business as durable, emphasizing its historical performance. Goldman has said it has not incurred losses on these types of loans, a claim that underscores its confidence in underwriting standards and collateral protections.

Growing Exposure to Private Credit

Goldman’s expanding ties to private credit reflect a broader shift in global finance, as alternative asset managers increasingly compete with traditional banks in lending markets. Firms such as private equity and credit managers have moved aggressively into financing leveraged buyouts and corporate transactions, often relying on banks for additional funding.

This interconnected ecosystem has raised concerns among policymakers and analysts. A recent report from a global policy group highlighted the rapid growth in borrowing by non-bank financial institutions, a category that includes private credit firms, hedge funds, insurers, and other alternative lenders.

At the end of last year, Goldman reported $118 billion in loans to such institutions, up from $91 billion previously, signaling a sharp increase in exposure.

Returns Reflect Pricing Power

While Goldman does not disclose detailed breakdowns of returns by borrower type, filings suggest that lending to these clients generates meaningful income. The bank reported $4.1 billion in interest income on average lending of $215 billion in the final quarter of last year.

Of that total, approximately $2.25 billion in interest was attributed to a portion of the loan book outside traditional categories such as real estate and consumer lending. On an annualized basis, this implies an interest rate of roughly 6.7%.

Although not all of these loans are tied to private credit, the majority of the exposure—more than 85%—is linked to non-bank financial institutions. The implied rate is broadly in line with high-yield bond markets, which averaged around 6.5% during the same period.

Market participants note that borrowers may be willing to pay a premium for Goldman’s execution capabilities, balance sheet strength, and reputation, even if financing costs are slightly higher.

Balancing Risk and Stability

Despite strong returns, the bank’s growing exposure to private credit has prompted debate over potential risks. Lending to non-bank financial institutions can involve layered leverage, where credit is extended to entities that themselves deploy leverage in underlying investments.

Goldman executives have sought to downplay these concerns. Chief Financial Officer Denis Coleman recently told analysts that worries about private credit risks are overstated, pointing to the firm’s track record of zero losses in this segment.

He attributed this performance to disciplined underwriting, robust collateral requirements, and risk management practices designed to protect the bank’s balance sheet.

Structural Questions Remain

Analysts caution, however, that historically low loss rates may not fully capture risks that could emerge in a more stressed environment. As private credit continues to expand and interconnections between banks and alternative lenders deepen, the potential for systemic vulnerabilities may increase.

The relationship between risk and pricing remains a central question. In traditional finance, higher interest rates typically reflect greater risk. Goldman’s ability to generate relatively high returns while maintaining minimal losses has raised questions about whether current conditions accurately reflect underlying risk levels.

Goldman Sachs’ lending to private credit clients highlights both the opportunities and complexities of modern financial markets. As banks and alternative asset managers become increasingly intertwined, the line between traditional and private credit continues to blur.

For now, the bank’s performance suggests that the model remains profitable and resilient. However, as market conditions evolve, investors and regulators are likely to monitor closely whether strong returns can be sustained without a corresponding increase in risk.

Stay informed with PE Newswire for authoritative coverage of global private capital markets, including the latest deals, fundraising activity, in-depth insights, and data-driven analysis.